Treat your public equity investments exactly like your private equity investments.

Originally published by Worth

By Garvin Jabusch

In his book The Inevitable: Understanding the 12 Technological Forces that Will Shape Our Future, Kevin Kelly writes, “We can embrace the current emerging shifts that will become the future…In a superconnected world, thinking different is the source of innovation and wealth.”

Once, managers of public stock portfolios viewed their job in this way; they invested client assets on the basis of what a given company did and its potential in the marketplace, then they patiently waited for those selected companies to fulfill that potential. Think Graham, Buffett, Lynch.

Today, public equity investing has become…not that. It is now about finding the lowest possible fee on an index, about indiscriminately owning the market so you don’t have to disambiguate the good ideas from the bad, the old from the new. The approach is lazy. In essence, indexing lets us shortcut full analyses in order to provide an option that we can readily justify in terms of economic activity as a whole, and in terms of fees. The idea of “I’m just investing in the economy” fails to recognize that the economy is comprised of entities that are growing and shrinking, better and worse, yesterday and tomorrow.

Via indexing, public stock investing has lost something crucial that only remains in the private equity or venture capital sphere. The only reason to look at a ticker is because the company it represents provides a solution to an economic need and ideally a solution to a systemic risk. It represents the evolution of the economy. Private equity seeks to get into a company early, before it is in an index.

Proactively searching for innovators and leaders does involve real work. It looks like this: You assimilate everything you know about the world, you decide a company is a leader in some aspect of its evolution, you conclude that the price is good for the risk and so you buy it. This usually results in investing in innovation, not legacy systems.

These often tech-leveraged innovations light the clearest path to long-term competitive portfolio performance because they provide more efficient and therefore more productive means of effecting legacy economic functions. As innovative approaches within each sector advance by improving economic productivity and steering away from unsustainable systemic risks, they will likely continue to gain market share from their risk-causing predecessors and therefore exhibit faster growth. Stock selection and economic context do matter.

The opposite of this—buying an index—means you’re left out of many of these newer opportunities, and worse, boxed into many of the legacy technologies they’re replacing. As I mentioned in a previous post, if you hold the S&P 500, you own at least 60 fossil fuel companies. You own companies whose products face shrinking demand, whose externalities threaten global economies and ecosystems, and whose replacements are among the fastest growing industries in the global economy. Bad call.

Why has it been difficult in recent years for many active managers to outperform indexes?

Some argue that active managers—even with “full” analyses (which will always be incomplete)—are unlikely to pick well, and therefore you’re better off with a passive, conventional index product that supposedly eliminates human bias. But why has it been difficult in recent years for many active managers to outperform indexes? Most active managers are trying to outperform their index, but are nevertheless adhering closely to that index in terms of tracking error. This is a severe limitation: If you’re trying to win a football game, but only win it by one point for fear of being labeled too volatile, you’re going to lose more often than a team trying to win by a higher margin. This is the trap of active management today.

So why do so many believe indexing is the alpha and omega of stock investing? Because it’s what we’ve been taught, and often all we’ve been taught:

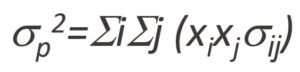

This formula is at the heart of Modern Portfolio Theory (MPT). It is how managers have defined risk for the past 65 years. What it represents is the covariance of the summation of the price performance histories between assets i and j. In other words, it defines risk as tracking error and, ideally, lack thereof. This has come to be interpreted to mean that the lowest risk portfolio is one that exhibits no variance from the mean, or from its index benchmark. High tracking error is said to equal poor risk-adjusted returns (even if absolute returns are good).

This is MPT’s key insight. Really. To be clear, this is not what Harry Markowitz, codifier of MPT, had in mind when he set down his rules in 1952, but it is in large part the current interpretation. And it is a big part of the inherited paradigm we all carry around in our heads, and one reason we have a hard time applying change and externalities to our models and portfolios. How strongly do managers, consultants and gatekeepers believe in this? So much so that scarcely anyone dares deviate from their mean. Because to do so is the very (supposed) definition of risk. So most managers remain, to varying degrees, boxed into the old economy via conventional index funds and funds that strive to track indexes closely.

And yet we all know that there are massive risks apart from covariance. Like technological obsolescence. Like climate change. Like resource degradation. By thinking about what a company actually does within the context of the global economy and real risk landscape (What does the company make? Does it create a solution to a systemic risk like climate change, or does it contribute to the risk? How and how well does it make it?), we gain a much clearer sense of risk than if we measured how far a given stock’s past performance varies from its peers or benchmark. Public equity managers can ignore benchmark correlation and instead seek the best ideas wherever they find them.

Theory is the foundation of application, so using a theory that no longer reflects reality results in a deeply flawed application. Present day interpretations of MPT are failing to adequately map the realities of the underlying economy and thus failing to protect investors from risk. Indeed, they end up exacerbating, rather than mitigating, risk.

So it is important to think hard about not only primary but secondary and tertiary consequences of how we make investment decisions. That’s a lot more difficult than falling back on indexing, but also potentially far more rewarding.

Think about what you own and if you believe it represents where the global economy is going. If not, why not? If you, like me, believe we’re in the midst of an unprecedented economic transition, but you nevertheless continue to hold legacy economy indexes, then you need to strongly reconsider how to bring those beliefs to life. It’s indeed an odd feature of people that we can end up arranging our priorities without considering the whole picture. Fortunately, we don’t have to. The rules of investing can be rewritten to prioritize the economy’s ability to thrive, as opposed to how well a portfolio correlates with some benchmark. This involves letting go of conventional wisdom and seeing the world afresh, like a private equity investor on the hunt for what’s next.

The world that bore us is changing; we need to adapt in kind. It’s time we started thinking and investing in our stock holdings like we were PE analysts—like we understand where the world is headed, and are no longer interested in where it’s been.

###

Important Disclosures https://greenalphaadvisors.com/about-us/legal-disclaimers/