How Goodhart’s Law Reveals the Opportunity in Long-Term Innovation Investing, and why traditional performance metrics may be undermining investment in transformative technologies – and how forward-thinking managers can turn this market inefficiency into alpha

As Chief Investment Officer of Green Alpha Investments, I’ve spent my career thinking about how market structures shape investment behavior, often in ways that create systematic inefficiencies. One of the most profound examples I’ve encountered is the application of Goodhart’s Law to modern portfolio management. When Charles Goodhart observed that a measure ceases to be effective once it becomes a target, he could have been describing my daily reality in managing portfolios that diverge significantly from conventional benchmarks.

The tension between benchmark-relative performance measurement and long-term innovation investing has been a constant theme in my work. I’ve watched countless portfolio managers succumb to the pressure of quarterly performance metrics against the S&P 500, leading to a form of institutional herding that I believe fundamentally undermines the market’s capacity to allocate capital efficiently to transformative innovations.

At Green Alpha, we’ve chosen a different path. Our focus on investing in solutions to systemic challenges – human disease, climate change, geopolitical risks – often leads us to earlier-stage companies with longer paths to maturity. These investments frequently fall outside major benchmarks and can experience higher short-term volatility. In my experience, these very characteristics, which make such companies unattractive to benchmark-hugging managers, create a systematic mispricing that patient investors can and do exploit.

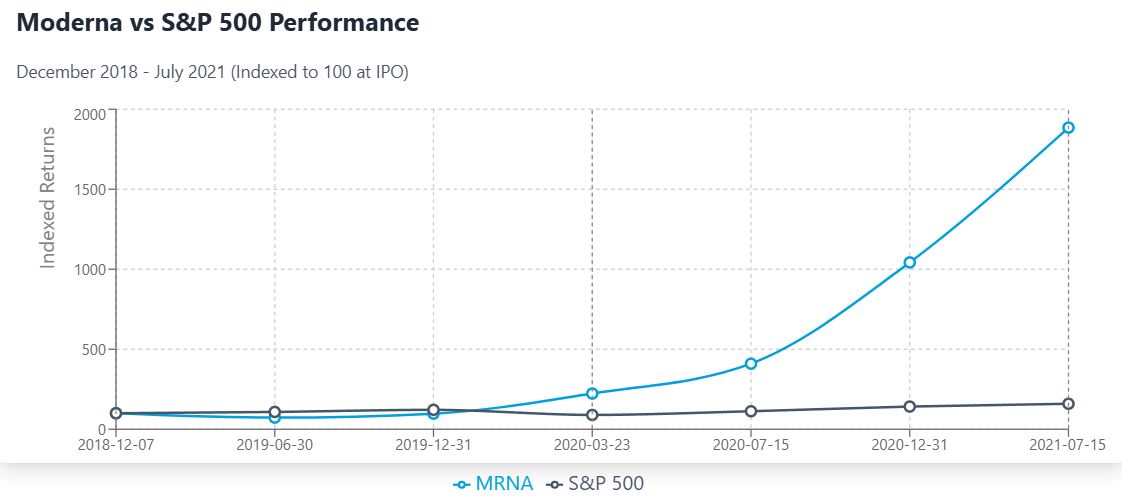

I’ve learned that the key is reframing both time horizon and risk. When we invest in transformative innovation, we’re thinking in terms of years or decades, not quarters. The biotech company Moderna’s journey offers a powerful illustration of this principle. In 2019, it was viewed by many as just another unprofitable biotech company with an unproven mRNA technology platform. By the time it was finally added to the S&P 500 in July 2021, early investors had already seen returns of 18 to 20 times their initial investment. This wasn’t just about the pandemic – it was about recognizing the transformative potential of mRNA technology and intellectual property ownership long before it became obvious to the benchmark-following crowd. Moderna’s story perfectly demonstrates how short-term price volatility can mask the emergence of paradigm-shifting innovation.

This perspective has shaped our approach to portfolio construction. Rather than viewing volatility as something to minimize, we see it as a natural consequence of investing in high-conviction ideas addressing fundamental challenges. Our position sizing reflects not benchmark weights but our conviction levels and company maturity. We achieve portfolio-level diversification not by matching sector allocations but through exposure to different types of systemic risks, innovations, technologies, and solution pathways.

Ironically, I’ve found that the very market inefficiencies created by widespread benchmark-following create our opportunity for superior long-term returns. As Goodhart’s Law would predict, when quarterly benchmark-relative performance becomes the target, it ceases to be a good measure of investment skill. I believe the truly skilled investor might be the one willing to accept higher tracking error, look beyond current index constituents, and maintain conviction through market cycles.

This approach requires both fortitude and clear communication with stakeholders. Over the years, I’ve spent countless hours explaining why conventional volatility metrics may be poor indicators of actual risk for transformative companies, and why patience through periods of underperformance may be rewarded. Most fundamentally, I’ve worked to help our investors understand that the purpose of investment management is not to track a benchmark, but to allocate capital to its highest and best uses, particularly to companies solving humanity’s greatest challenges.

The final irony may be that by explicitly rejecting benchmark-relative performance as a primary metric, we believe we can ultimately deliver superior long-term results. In this way, understanding and adapting to Goodhart’s Law becomes not just an academic exercise but a source of competitive advantage in investment management. It’s a principle that has guided my investment philosophy throughout my career, and one that I believe becomes more relevant with each passing year.

###

Green Alpha is a registered trademark of Green Alpha Advisors, LLC. Green Alpha Investments is a registered trade name of Green Alpha Advisors, LLC. Green Alpha also owns the trademarks to “Next Economy,” “Investing in the Next Economy,” “Investing for the Next Economy,” “Next Economy Portfolio Theory,” and “Next Economics.” Green Alpha Advisors, LLC is an investment advisor registered with the U.S. SEC Registration as an investment advisor does not imply any certain level of skill or training. Nothing in this post should be construed to be individual investment, tax, or other personalized financial advice. Please see additional important disclosures here: https://greenalphaadvisors.com/about-us/legal-disclaimers/

At the time this article was written and published, some Green Alpha client portfolios held long positions in Moderna (ticker MRNA). These do not represent all of the securities purchased, sold, or recommended for advisory clients. You may request a list of all recommendations made by Green Alpha in the past year by emailing a request to any of us. It should not be assumed that the recommendations made in the past or future were or will be profitable or will equal the performance of the securities cited as examples in this article. Not all Green Alpha separate accounts or our sub-advised mutual fund held the stock mentioned. To inquire whether a specific Green Alpha portfolio(s) holds stock in any particular company, please call or email us.